Originally published March 2025 – updated April 2026 to reflect new research and a tighter structure.

Introduction

Most people who invest believe they are keeping pace with the market. Not beating it – few expect that – but roughly tracking it. The evidence, accumulated across three decades and multiple continents, says otherwise. The gap between what markets return and what the average retail investor actually captures is not a rounding error. Compounded over a working lifetime, it is the difference between financial independence and a number on a retirement statement that falls well short of the plan.

What makes this uncomfortable is that the gap is not random. It is systematic and predictable, appearing in the United States, Taiwan, Europe, and Brazil, across bull markets and bear markets alike. The causes are not external. They are structural, behavioral, and for the most part fixable.

The Performance Gap Is Real, and It Is Large

Start with the numbers. The DALBAR Quantitative Analysis of Investor Behaviour tracks what the S&P 500 returned against what the average equity fund investor actually earned. Over 30 years, the index compounded at roughly 10.65% per year. The average investor earned 7.13%. That 3.5 percentage point annual shortfall sounds manageable. Applied to a USD 100,000 starting investment, it means the difference between approximately USD 800,000 and USD 2,000,000 at the end of three decades. Same market. Same period. Radically different outcomes.

The pattern holds internationally. A landmark study of Taiwan’s stock market found individual investors underperformed by 3.8 percentage points per year after costs, consistently, across market cycles. In leveraged derivative markets the numbers are bleaker still: ESMA data shows 74% to 89% of retail CFD clients lose money; not occasionally, but as a structural outcome.

DALBAR also records that the average holding period for equity funds is around four years. In a market that rewards patience across decades, that tenure is barely enough to smooth a single downturn. The underperformance gap and the short holding period are not coincidental.

Behavioural Biases: The Primary Driver

The dominant causes of underperformance are psychological. Overconfidence is the starting point. The Barber and Odean study of 66,000 brokerage accounts found that the most active traders lagged the market by 6.5 percentage points annually, while men who traded 45% more than women in the dataset, underperformed by 2.65 points per year. Higher conviction produced higher turnover, which produced lower returns. The trading was the problem.

The disposition effect compounds it: investors sell winners too early (gains feel good to lock in) and hold losers too long (realising a loss feels like failure). Research consistently shows a roughly 60/40 ratio of winner-to-loser sales; the precise opposite of what tax efficiency and momentum would suggest.

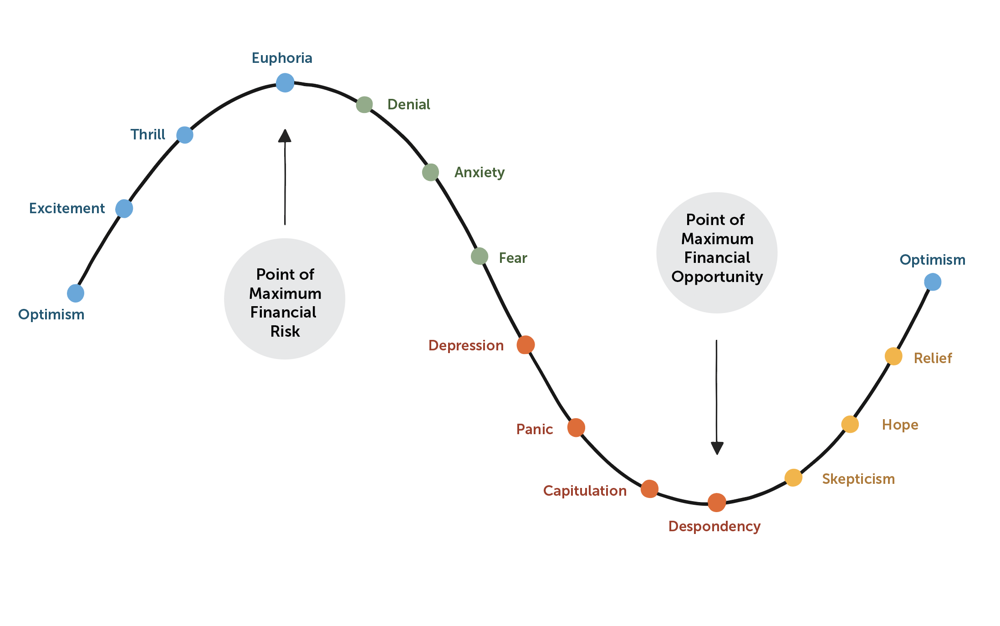

Then there is the emotional cycle. Markets attract peak retail participation near tops, when risk-reward is worst, and maximum fear near troughs, when expected returns are highest. The result is the predictable pattern: buy high on excitement, sell low on panic. FOMO, the fear of missing a trending asset, is this same cycle with a social media amplifier, visible in every episode from GameStop to late-2020 crypto. The asset changes; the mechanism does not.

For how this dynamic plays out at its most extreme, look out for my upcoming post on why day trading can be closer to gambling than investing.

The Diversification Trap

Diversification is perhaps the most widely understood concept in investing and one of the least practiced. Wharton research on home bias documents that most retail investors hold far less international exposure than optimal allocation theory supports. Not because of a deliberate view, but because familiar markets feel safer. They are not.

Concentration risk is not abstract. Enron employees with heavy company stock in their retirement accounts and Lehman bondholders who treated investment-grade ratings as a substitute for diversification discovered this in the most direct way possible. The deeper issue is that overconfidence and home bias reinforce each other: familiarity breeds confidence that is rarely backed by genuine informational advantage. Knowing a company makes popular products does not give a retail investor any edge over the market’s collective assessment of its equity.

The Cost Drag Nobody Talks About

The single best predictor of whether a fund will outperform its benchmark is not the manager’s track record, the fund rating, or the sophistication of the strategy. It is the expense ratio. Morningstar’s research has found this repeatedly: low fees predict future outperformance more reliably than any other observable variable. Fees are certain; alpha is not and most actively managed funds do not deliver it.

The compounding effect of fees is routinely underestimated. A 2% annual expense ratio on a fund earning 8% gross does not reduce your return by 2%. Over 30 years, it reduces your ending portfolio value by roughly 40% compared to a 0.1% index fund alternative. Put differently: a significant portion of your accumulated wealth transfers to the fund manager in exchange for, in the majority of active fund cases, worse performance than the index it is supposed to beat. Transaction costs such as spreads, short-term capital gains tax, and payment-for-order-flow frictions compound the drag further. The damage does not appear on any individual trade confirmation, but it is plainly visible in long-run net returns.

The Structural Disadvantages Are Permanent

Even a retail investor who resolved every behavioral problem above being fully rational, diversified, and cost-conscious, would still face structural headwinds. Institutional players have faster execution, lower transaction costs, dedicated research analysts, and direct access to company management. They operate at scale that generates better pricing on every trade and access to private placements, block deals, and research simply unavailable to retail participants. These advantages are structural and permanent. They cannot be closed through effort or study.

The correct response to a game where the structural odds are permanently against you is not to try harder at it. It is to stop playing it on those terms. Practically, that means:

- Replace stock-picking with low-cost index funds: capture the market return that, as the DALBAR data shows, most active retail investors never achieve.

- Extend your time horizon deliberately. The four-year average holding period is far too short for compounding to work; think in decades.

- Automate contributions and rebalancing (see my post on paying yourself first). Removing discretion is the most effective defence against behavioural bias.

- Minimise costs relentlessly: expense ratios, turnover, and tax drag are the only components of long-run return you can control with certainty.

The market is not the obstacle. It has rewarded patient, diversified, low-cost participation handsomely over every multi-decade period on record. The obstacles are the behavioral tendencies, cost structures, and mistaken beliefs that most retail investors carry into it. None of which are inevitable, and most of which have straightforward remedies that require less activity, not more.

The harder question is not what to do. It is whether you are honest enough to recognize which of these patterns applies to your own portfolio and to act on that before another compounding decade passes.

Final Thoughts

- The average retail investor has underperformed the S&P 500 by roughly 3.5 percentage points per year over 30 years; a gap worth more than USD 1.2 million on a single USD 100,000 investment.

- Overconfidence and overtrading are the primary culprits: Barber and Odean found the most active traders lagged the market by 6.5 points annually; the Taiwan market study shows an identical structural drag on all individual investors.

- Emotional timing and the disposition effect systematically lock in losses and surrender gains; FOMO is the same mechanism with amplified stakes.

- Concentration and home bias substitute familiarity for genuine risk management; Wharton’s research shows most retail investors are less diversified than they believe.

- Fees are the most reliable predictor of fund performance: Morningstar’s data shows low costs beat active manager selection, consistently, over the long run.

- The most effective strategy is the least exciting one: low-cost index funds, automated contributions, long time horizons, and the discipline to leave the portfolio alone.